As market conditions present volatility and uncertainty, companies are increasingly viewing 2023 as a year to prepare for entry into the public markets in 2024 or beyond. While an IPO may be more than a year away, various workstreams and activities can be started in the short term to help successfully execute a public offering more efficiently and to establish strong corporate governance.

Below we discuss a selection of the more time-sensitive activities, which can enable companies to evaluate where they currently are in their journey to operating as a public company.

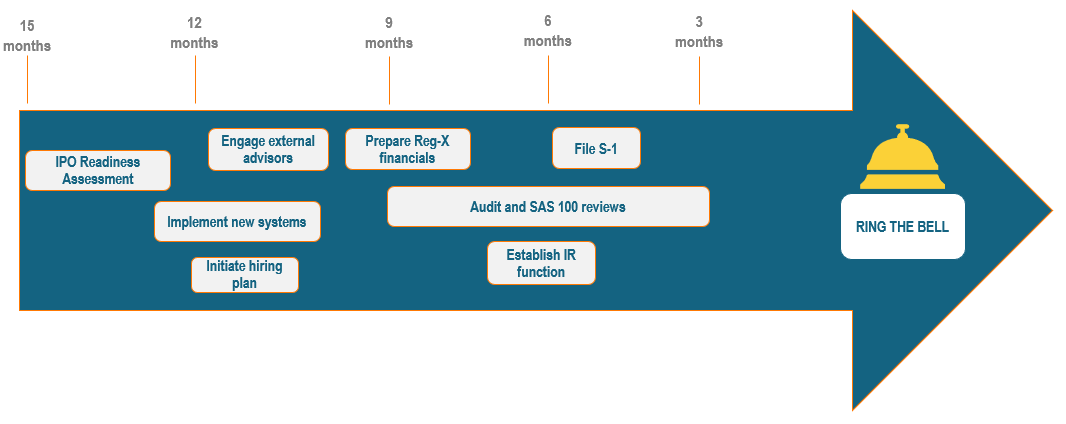

IPO Timeline and Activities

1. IPO Readiness Assessment

A comprehensive readiness assessment provides a tailored roadmap that bridges a company’s current state of operations to an operating model that will enable the company to perform effectively as a public company. The assessment also can facilitate internal discussion with the Board of Directors, Audit Committee, and executive team with the goal of aligning the company’s priorities ahead of a public company listing.

2. Engage External Advisors

A company pursuing an IPO will need to engage a variety of new advisors and third parties to successfully execute the transaction. These can include accounting advisors, SEC counsel, investor relations firms, underwriters, HR and compensation consultants, and valuation and tax specialists. Determining suitable advisors for your company prior to kicking off the IPO process can enable a more efficient transaction and provide time for the company to do an appropriate level of due diligence.

3. Implement New Systems

Companies burdened by legacy systems and processes can benefit from an evaluation of their current technology landscape. By identifying inhibitors, implementation partners can design and deploy future-ready automation and data solutions that improve operational efficiency, which is vital to meeting public company rigor.

Deliver value in the deal and beyond with expert IPO filing and advisory solutions

Generate and protect a profitable public company state with a methodology focused on your organization’s critical financial, operational, and technology-related functions.

4. Initiate Hiring Plan

A private company will typically need to build out teams and functions to meet its strategic growth plan along with the demands and governance requirements of a public company. By assessing current staff and competency levels versus a public company environment, leaders can provide sufficient runway to complete their hiring plan and onboard employees ahead of the IPO.

5. Prepare Regulation S-X Financial Statements

Upgraded financial statements that meet the Regulation S-X disclosure requirements will be needed for any prospective S-1 filing. CFOs and Controllers may want to consider whether upgraded statements should be prepared in conjunction with their current-year audit to facilitate inclusion in a future S-1 filing. This approach limits the “uplift” and additional audit work that may be required on the financial statements when the S-1 registration statement is being prepared.

6. Audit and SAS 100 Reviews

Private companies under an American Institute of Certified Public Accountants (AICPA) audit opinion should liaise with their external auditors to determine when a Public Company Accounting Oversight Board (PCAOB) audit is appropriate for their current circumstances and future IPO plans. Additionally, companies should discuss with their external auditor the timing of interim SAS 100 procedures over their quarterly financial information. The periods to be included in a prospective S-1 filing will inform the company as to which quarters may be subject to SAS 100 procedures.

7. Evaluate SOX Preparedness

While smaller reporting companies and emerging-growth organizations have some accommodations with regard to SOX compliance, it’s still essential that internal control standards be made more robust, particularly as they relate to compliance requirements for Internal Controls Over Financial Reporting (ICFR).

As a first step, conducting a SOX risk assessment and scoping exercise can ensure key processes and systems are identified and documented. This strategic planning exercise focuses the company on the most significant and critical processes supporting financial reporting. Once key processes are identified, assess the state of internal controls and remediate control gaps where necessary. Starting with common high-risk processes, such as Revenue, Financial Reporting, and IT General Controls, is a good place to start. Delaying improvements to a company’s internal control environment can increase the risk of a material control weakness.

On the IPO journey, at no point should you be standing on the sidelines waiting for markets to play out. Due to the variety of organizational and regulatory activities required over the course of more than a year, starting the journey now can ensure optimal IPO readiness when the day does finally come.

For expert IPO readiness support, contact Biovell today.