In most corporate divestitures or spins, there’s considerable complexity involved in the preparation of carve-out financial statements for the divested business. Because transactions requiring these statements are unique and nuanced, they necessitate the use of specialists versed in the subject matter.

What Are Carve-Out Financial Statements?

Carve-out financial statements are documents prepared to reflect the financial information of a particular business, such as a segment, business unit, or product line. This carve-out financial information is derived from the parent’s historical financial information and is usually needed when a company intends to pursue a divestiture, such as through a sale to investors, a spin-off to existing shareholders, or an initial public offering. Entities prepare carve-out financial statements for investors to gain a better understanding of the business, which may then be used in:

- Due diligence activities.

- Marketing materials for the sale of the business.

- Building valuation models.

- Satisfying public financial reporting requirements.

It must be highlighted that carve-out financial statements are not always subject to external audit, especially in instances where a business is divested through a private sale (e.g. a private buyer).

Acquirers may need to provide audited financial statements under the requirements of SEC S-X Rule 3-05 for lender purposes or if an acquisition is significant for a buyer. Sellers should complete the significance test (under Rule 1-02(w) of Regulation S-X) on the buyer pool to determine whether the business to be divested potentially meets the SEC significance test for these potential buyers. If a business is considered to be a significant acquisition for a buyer, SEC-compliant audited financial statements may be required for one to a maximum of two years, as may the latest unaudited year-to-date interim period (along with the comparative period) for an acquired business.

Below are five common misconceptions encountered when preparing carve-out financial statements and how to deal with them.

1. Preparing Carve-Out Financial Statements Is Straightforward

The preparation of carve-out financial statements will always present certain complexities that may require input from multiple stakeholders involved in a proposed transaction. These reasons include:

- The limited accounting guidance available on the preparation of carve-out financial statements.

- Decisions made for a parent company will need to be evaluated through a different lens for the carve-out entity (e.g., sufficiency of historical accounting policies and disclosures).

- Financial information previously audited as part of the parent entity (e.g., cash flows, assets, liabilities, and other key financials) may be subject to additional audit procedures due to lower materiality thresholds for the carve-out entity.

- Performance of an in-depth analysis to determine what additional costs should be allocated and included in the carve-out financial statements is required even for an entity or segment that is operating separately from its parent.

In practice, preparers refer to SEC guidance and carve-out guidance published by external advisory firms when preparing carve-out financial statements. Such guidance requires these statements to reflect all of the costs of doing business historically, including directly attributable costs and an allocable share of corporate costs. However, given the limited guidance available, there is often divergence in the treatment of individual items, making an SEC filing or other corporate finance transactions complex.

The ease with which such financial information can be extracted from the entity’s historical financial information depends on how the specific data/accounting records were captured for the business being divested. For example, is information for the business discrete from or heavily intertwined with the parent entity? The more intertwined they are, the more time required to perform an analysis of the discrete financial information to be included in the carve-out financial statements. In general, balance sheet preparation is where most entanglement of accounts is experienced, especially with shared customers and suppliers between RemainCo and DivestCo.

Explore expert Divestiture & Carve-Out solutions that solve real-world problems

Maximize shareholder value, ensure a profitable path forward, and proactively manage complex accounting, risk, and systems implications for RemainCos and NewCos.

2. Historical Financial Reporting Alone Is Sufficient to Prepare Carve-Out Financials

Historical financial reporting is the basis for preparing carve-out financial statements. Nevertheless, preparing these statements requires a detailed analysis to determine which assets, liabilities, profits, and losses to include.

When determining the assets and liabilities (which are generally recognized entirely or not at all) to include on the balance sheet, consideration is given to legal rights and obligations — such as ownership of the asset or requirement to settle the liability — as well as the entity’s shared use of an asset or liability. Additionally, decisions from management will also play a role here as, for example, decisions are often made for transactions such as spin-offs to result in a debt- and cash-free entity being spun-off, which will result in historical financial statements also reflecting this position.

Because the income statement should reflect all costs of doing business, when determining the profits and losses to include, preparers must consider items specific to the carve-out entity and to an expense allocation for corporate or shared service costs. Tax-related balances included in the carve-out financials must also be prepared on a separate provision basis. This will usually result in a different effective tax rate from the former parent company due to a different jurisdictional mix along with the possibility of group legal entities previously not considered as part of a tax group or single filer now being included in the computations.

3. Carve-Out Financials Are the Same as Deal Basis Financials

The same underlying carve-out financial information will provide the foundation for both Deal Basis and Audit Basis Financial Information. However, the deal and audit basis ultimately are different in nature.

Deal Basis financials are generally used to aid the seller in providing a normalized and pro forma view of the business as a standalone go-forward business, allowing potential buyers to better understand historical results on a normalized performance basis. The Deal Basis financials will also help provide the basis for the divested business’s forecasted financials.

As Deal Basis Financial Information is non-GAAP in nature and unaudited, preparers have more flexibility in making pro forma adjustments to illustrate the impact of items like one-time costs. Preparers of Deal Basis financials are not constrained by carve-out guidelines regarding assigning assets and liabilities, or allocation methodologies for costs. However, the Deal Basis financials will go through the due diligence process completed by potential buyers. The historical and pro forma quality of earnings adjustments will be challenged during this diligence process. As such, adequate arguments and documentation need to be provided or there may be adjustments identified as part of the due diligence process.

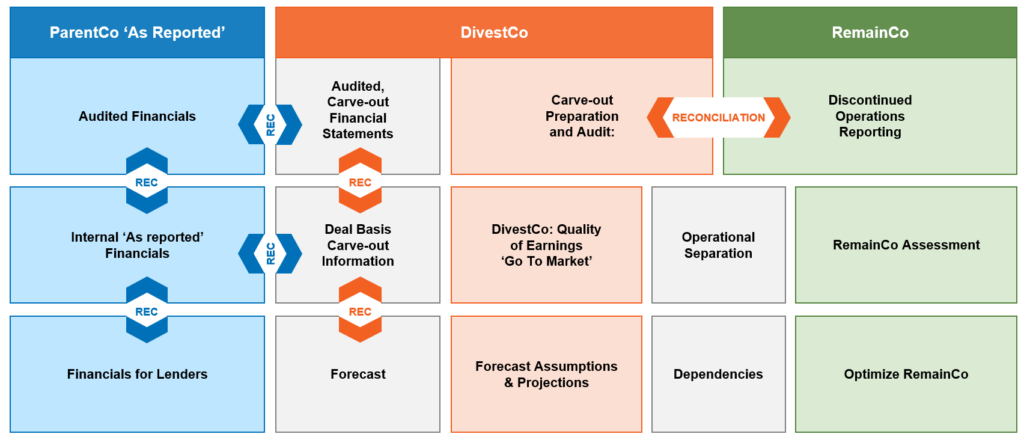

The base system and management reporting information are the same for all types of carve-out financial information. It’s critical to be able to explain, reconcile, and bridge the various pieces of carve-out information as laid out in the graphic below.

4. Historical Allocation Methods for Shared Costs Are Appropriate

It’s common for companies to internally allocate corporate costs incurred by the parent to their segments, subsidiaries, or product lines. The methodologies employed for historical internal allocations reflect those that management considered were the most appropriate at the time. However, these methodologies should be analyzed to ensure they reflect the true historical cost of doing business for the carve-out entity, and, in most instances, additional costs will need to be allocated. However, in limited cases, the historical allocation will be appropriate, especially for certain regulated businesses that require full allocation to each business.

A key determinant of costs to be allocated is ensuring that there is an accurate pool of historic corporate costs established. It’s common for this pool to include expenses not historically allocated across the business, such as corporate HR, Legal, IR, IT, and FP&A costs, all of which would be applicable for a standalone company. Once an accurate pool of costs has been determined, preparers will need to ensure that allocation methodologies and calculations are reasonable, consistent, and auditable, while also being in line with guidelines provided by the SEC.

5. Historically Reported Segment Will Equal the Carve-Out Entity Results

While in some transactions the carve-out entity may comprise components of multiple segments, when an existing segment is carved out in full, the results and balances will rarely be the same as those historically disclosed by the former parent. Differences are caused by the application of carve-out accounting, management decisions, and allocations of shared costs, none of which may be considered in the segment reporting of the former parent.

An additional challenge often faced when preparing carve-out financial statements is the determination and disclosure of reporting segments of the carved-out entity if this disclosure is required (e.g. Spin/IPO). In some cases, it’s appropriate to have one reportable segment; however, it’s also very common for a segment determination analysis to be completed for a carved-out entity and additional reportable segments identified. Entities should pay close attention to the segment guidance in their analysis and apply accordingly as this has been an area of focus for SEC reviewers in recent years. It must also be noted that carve-out financial statements produced for use in a private sale or to satisfy significance requirements (S-X Rule 3-05 financials) do not require segment disclosures.

For expert carve-out accounting guidance, contact Biovell today.